For many people taxation is a confusing minefield in Spain, this is a simple Guide to the different taxes that residents and non residents are liable to pay annually.

1. IBI (Impuesto sobre Bienes Inmuebles, similar to UK Council Tax) and often called SUMA, although that is the name of the agency which collects the tax"

This is a local tax which the Council imposes on all property owners based on the cadastral value of the property. The notification for the IBI bill is posted out directly to the property by the Suma Office , usually paid by early September but delayed in 2020 to November due to the Covid-19 situation.. If on direct debit, you need do nothing. If you have not set up a direct debit, then the notification has a slip at the bottom and should then be taken to be paid at any of the participating banks.

2. Income Tax for Residents.

Calculation and payment of the Individual Income Tax can be a complicated business. Individuals are deemed as Residents if they meet any of these conditions:-

they spend more than 183 days per calendar year in Spain

their main place of business is indirectly or directly located in Spain

Residents are taxed on worldwide income although UK Government Pensions while having to be declared on your Spanish Tax Return are not taxed in Spain as they are taxed in the UK. If you are renting out a property as a short term / holiday let quarterly Tax Returns must be submitted, if renting out your property as a long term let an annual Tax Return is submitted. Given the complexity of completed a Tax Return I would recommend that you employ a Abogado to complete the return for you.

Article continues below

3. Non Resident Tax.

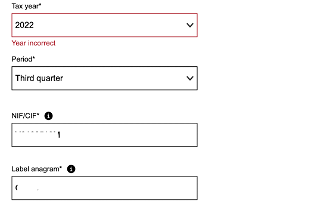

Non-Resident tax is the commonly used term for the tax on Non-resident Spanish property owners. This is due to be paid individually whether or not their property in Spain is rented out. As with Income Tax for residents non residents must submit Income Tax Returns in relation to income if their property is rented out at any time. Again you can complete your Tax Return yourself or employ a specialist company. When we were non resident we used Spanish Tax Forms Limited ( https://www.spanishtaxforms.co.uk/ ), payment of a modest fee and they completed all the necessary paperwork, emailed it to us and we printed it off to take to our Bank to pay the tax, the following year we had the confidence to complete it ourselves.

4. Capital Gains Tax.

When yo sell a property in Spain you have to pay Capital Gains Tax on any profit after taking into account all deductions and allowance. My opinion is that professional assistance is essential as this is such a complicated issue.

5. Inheritance Tax.

Article continues below

Inheritance Tax, also called Succession Tax ( impuesto de successions y donaciones) is one of the main taxes paid in Spain by both residents and non residents. It is a progressive tax paid by the individual who receives an inheritance from a friend or relative, being a property, money or any other kind of asset.

6. Car Tax.

Paid through the Suma Office by the registered owner of the vehicle on the 1st of January for the whole year.

7. IVA ( VAT)

IVA ( in Spanish: impuesto sobre el valor añadido or impuesto sobre el valor agregado), equivalent to VAT, is due on any supply of goods or services sold in Spain. The current normal rate is 21% which applies to all goods which do not qualify for a reduced rate or are exempt. There are two lower rates of 10% and 4%. The 10% rate is payable on most drinks, hotel services and cultural events. The 4% rate is payable on food, books and medicines.

8. Plusvalia Tax.

Plusvalia is a Local Tax, so it’s produced by the Town Hall where the property is located, the Tax is also called “Impuesto Sobre el Incremento de Valor de los de Naturaleza Urbana”. It is a Tax generated when someone transfers a property either via sale, donation or inheritance. Once the transfer has been completed you are notified by a letter of payment. Many times, the buyer calculates the full amount and withholds this quantity (from the amount of the purchase) to pay on the sellers behalf (this usually happens when the seller is a Non-Resident).

.In February of 2017, the Constitutional Court annulled the Plusvalia Tax and, in another May ruling, established that taxpayers should not pay such tax when the sale of the house has generated losses although many Town Halls still demand payment of the tax. Since then the Supreme Court clarified that you can only claim the return and the Plusvalia Tax in cases where it can be proved that there were losses. That proof are property deeds, both, acquisition and transfer deeds. As you can see this is an extremely complicated situation and professional advice is essential.

Written by

Spain Tips and Guides: your complete guide to visiting, living and moving to Spain

Spain Tips and Guides: your complete guide to visiting, living and moving to Spain